Credit Score Basics

What is a Credit Score?

You probably already understand the Credit Score basics, like how failing to make a payment will cause your scores to drop, but there are a number of credit scoring complexities which still trip up the average consumer. If you pay your debts on time, do not carry too much credit card debt (especially on one individual credit card), do not close older accounts unless absolutely necessary, and only apply for new credit when you really need it you will generally have credit scores which remain in good shape. However, it is extremely important to keep yourself well informed so that you can maintain your good credit scores in the future as well.

Credit scores, a separate product from your credit reports, make the job of screening candidates much easier for lenders to standardize and monitor efficiently. FICO scores specifically (the brand most used by lenders) are designed to predict the likelihood of you becoming 90 days late on any account within the next 24 months. Lenders reply upon both your credit report(s) and credit score(s) to judge your reliability as a loan candidate. Your credit indicates your ability to handle debt responsibly and can help banks decide if you are a desirable loan customer.

Higher credit scores can help you in a variety of ways such as locking in low APR rates or securing special deals on financing. Conversely lower credit scores may prevent you from securing loans at all, damaging your ability to purchase a car, open a credit card, qualify for a mortgage, or even rent a home or apartment. Poor credit scores (generally caused by a credit history which reflects an inability to manage credit successfully) will often make lenders uncomfortable about trusting you with additional funds in the future.

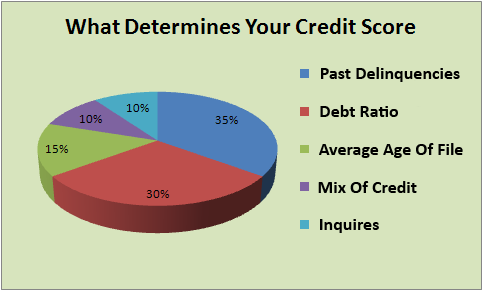

What Makes Up a Credit Score?

Your FICO credit score, created by the Fair Isaac Corporation, is determined by a complicated algorithm. Three separate corporations known as the “credit bureaus” specialize in collecting and reporting data about your financial history. The three major credit bureaus in the US are known as Equifax, TransUnion, and Experian.

While the exact formula used to calculate your credit score with each credit bureau is a closely guarded industry secret, FICO does provide some general guidelines about how your financial behavior may affect your credit score.

FICO Credit Score Components

1. Payment History: 35% of Your Credit Score

This category of your credit should really be referred to as the “presence or lack of derogatory information.” FICO’s credit scoring models are designed to ask questions of your credit reports. For example: Are any late payments present? If the answer is yes then you will earn less points to be added to your overall credit score than you would have earned if there were no late payments present on your report.

When it comes to negative marks like late payments, collections, etc. FICO’s credit scoring models will focus on 3 factors:

- Delinquency – This is the last time you were late.

- Frequency – Someone with 1 late looks better than someone with a dozen late payments.

- Severity – A 30 day late payment is not as serious as a 60 day or 120 day late payment. Collections, tax liens, judgments, and bankruptcies are all considered to be severe delinquencies and are also known as “credit score killers.”

2. Amounts Owed: 30% of Your Credit Score

FICO’s credit scoring models also pay a lot of attention to the amount of debt you owe. Factors considered include how much you owe on each account as well as how much you owe on different types of accounts (mortgage, auto, credit card, etc.). Special attention is paid to how much credit card debt you carry and how that debt relates to your credit limits (aka your revolving utilization ratio). The formula used to determine your revolving utilization ratio looks like this: $870 balance / $1,000 limit = 87% utilization.

To make a long story short, using a higher percentage of your credit limits will worry lenders and harm your credit scores. Consumers who max out their credit limits are especially concerning to lenders as statistically they represent a much higher risk of default.

The bigger the gap between your credit card balances and your credit card limits, the better.

3. Length of Credit History: 15% of Your Credit Score

This category is certainly less important than the first 2 which have been mentioned, but still relative and influential over your credit scores. It is possible to have a good credit score with a short credit history, but the longer you have had credit established the better the impact will be upon your scores. FICO’s scoring models consider the following factors within your “Length of Credit History” category:

- The Age of Your Oldest Account

- The Average Age of All of Your Accounts Combined

4. Mix of Credit: 10% of Your Credit Score

FICO’s scoring models are designed to reward consumers who have a healthy mix of credit, but the company remains a bit vague on what this actually means. It is recommended that you have a balance of both revolving accounts (think credit cards) and installment accounts (think auto loans, mortgages, and personal loans) in order to maximize your credit scores within this category.

5. New Credit: 10% of Your Credit Score

Applying for and opening new accounts has the ability to ding your FICO credit score, particularly if you have applied for a lot of new credit within a short period of time and do not have an otherwise lengthy credit history. The following factors are considered within this category of your credit reports:

- How Many Accounts You Have Applied for Within the Past 12 Months

- How Many New Accounts You Have Opened

- How Much Time Has Passed Since You Applied for Credit

- How Much Time Has Passed Since You Opened a New Account

The best rule of thumb is to only apply for new credit when you really need it.